One strategy designed to minimize downside risk is to marry a long

multi-month Put with a long stock position. If the stock value drops, the

long Put compensates for it. The position's risk profile looks like

the following chart, kind of like a hockey stick profile: limited downside

coupled with unlimited upside. Typically, putting this position on and leaving it until the Put expires has

a 70% chance of losing money. The key to this strategy is the

adjustments one makes to take cash from the position, i.e., to eliminate the

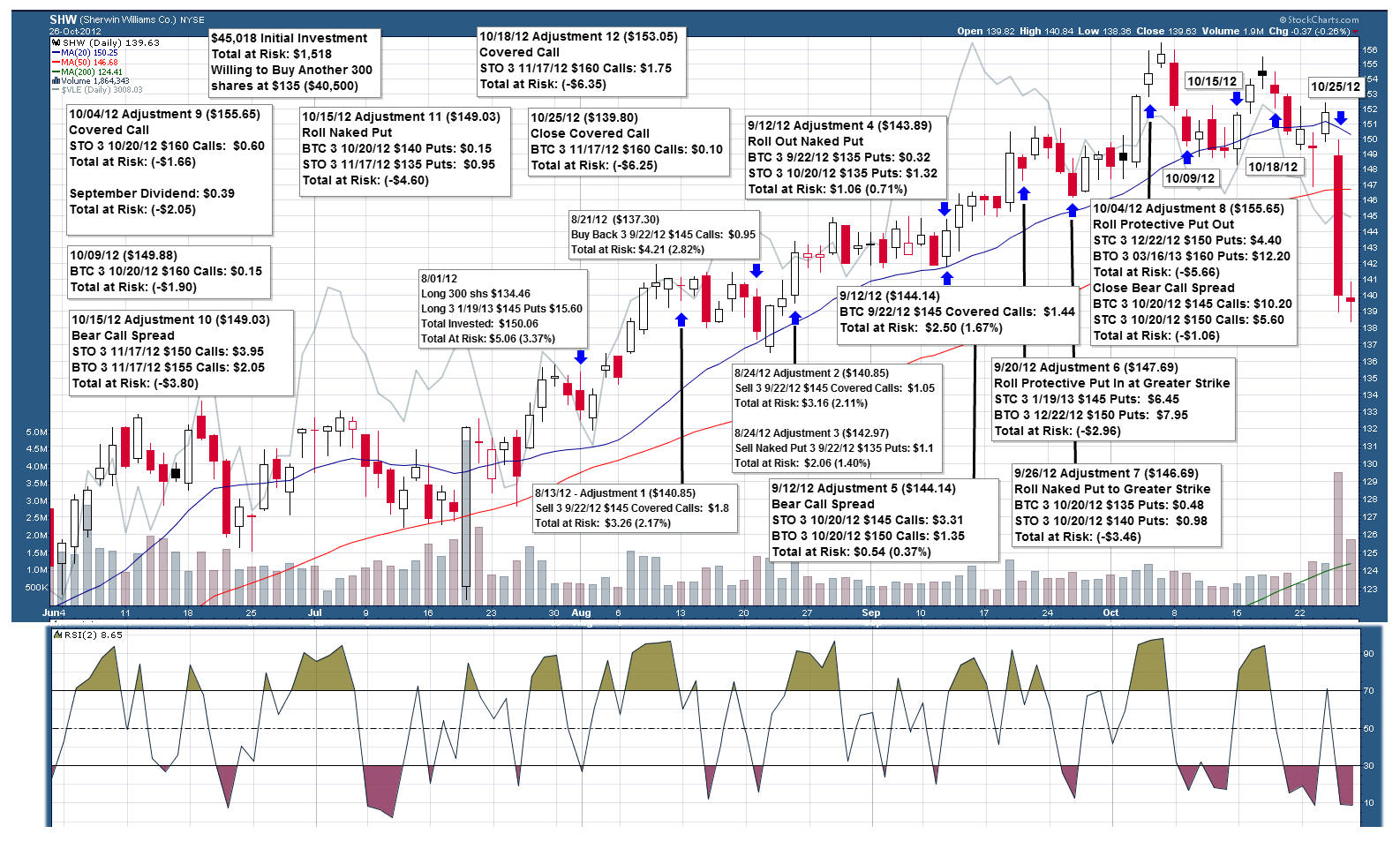

red in the chart. Consider an example that I currently am holding with SHW,

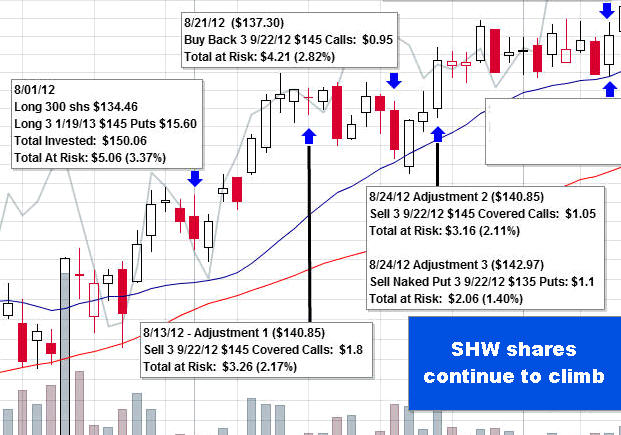

On 8/01/12, I bought 300 shares of SHW at $134.46 a share

and three $145 Strike Put contracts that would expire on 1/19/13 (six months

away) at a price of $15.60. My total investment was $150.06 per share

or $45,018. You might ask: Why would you invest $150.06 per

share when SHW was trading at $134.46? That's a good question, let me

show you why.

Here's another way to look at the trade:

Cost per Share for SHW : $134.46

Cost per Share for $145 Put : $ 15.60

Total Cost per Share for SHW :

$150.06

Guaranteed Sale Price from Put : $145.00

Total at Risk :

$ 5.06 or 3.37% ($5.06/$150.06)

At this point, I

have just 3.37% of my investment at risk ($1,518).

That's the orange area

of the hockey stick risk profile. SHW could drop to zero, and I would only

lose the 3.37%. Over this six month period, my upside is anything above

$150.06. My immediate goal is now to eliminate the

$5.06 at risk as quickly as possible: by selling covered calls, by

selling naked puts, by collecting dividends, by moving the protective put up

or down as the position evolves, and by putting on various spread trades.

Note, I view this initial position as half a position. The second half

will be purchased if/when a naked Put puts more shares to me.

On 8/13/12 (12 days later), the first position

adjustment was made with SHW shares trading at $140.85 (after a

$6.39

advance). Three $145 covered calls were sold that would expire on

9/22/12 (40 days away). The premium was $1.8, which immediately reduced my $5.06

to $3.26 a share. Now 2.17% of my investment remained at risk. Note, instead of selling

the covered calls, I could have closed the position to capture most of the

$6.39 advance: selling the shares and the three Put contracts and at

no time during the trade would I have been exposed to more than my original

3.37% risk.

The chart below shows how this investment evolved through 12

adjustments by 10/25/12 to completely eliminate all its risk. Better

than that, in fact, to guarantee that I would receive a minimum of $6.25 per

share with unlimited upside from that. Over the next few weeks, I'll

describe each of these adjustments in turn.

Note, if you're interested in learning more about this

strategy, known as a Married Put, visit the radioactivetrading.com site.

My original contribution to this strategy is marrying the TSM stock pick to

the married Put position to control, even eliminate all downside risk.

That is, I identify quality stocks with remaining value and trade them with

a strategy that controls, even eliminates risk.

On 8/21/12 (8 days later), SHW shares dipped down to $137.30 and the

Covered Call $145 shares were bought back for $0.95 a share which raised my

risk to $4.21 (2.82%). This completed the first income

producing cycle.On 8/24/12 (3 days later), SHW shares rebounded

higher (to $140.85) and Adjustment 2 was made: three $145 strike

Covered Calls were sold for $1.05 per share to expire on 9/22/12 (now 29

days away). My risk is now $3.16 (2.11%). This could obligate

me to sell my 300 shares for $145 a share should the buyer want me to, but

$145 would be at a nice profit, and my long $145 Jan Puts could then be sold

to recover much of its $15.60 original cost. Of course, I hope SHW pulls back

to enable me to buy the Calls back or that they expire worthless.

Later in the day on 8/24/12, Adjustment 3 was made as

shares climbed to $142,97: three $135 Naked Puts were sold to expire

on 9/22/12 (in 29 days), and $1.10 premium was taken in reducing my risk to

$2.06 (1.40%), i.e., the total amount that I could lose--even if SHW

shares dropped to zero--would be $630. These Puts could require me to

buy the second half of my position should the SHW share price drop 5.6%.

From my perspective, I would not mind buying these additional shares at that

price. Of course, I'm hoping that SHW shares don't drop, but these

Puts expire worthless, and the premium just serves to reduce my risk.

These adjustment's sole purpose is to reduce my risk of owning the original

300 shares (the downside risk) and continue to participate in the run higher

of this quality TSM (TripleScreenMethod) stock (the unlimited upside

potential).

In summary to this point, I'm 24 days into the SHW trade.

Its price has risen from $134.46 to $142.97 (up $8.51).

My basis is now $134.46 + $15.60 - $1.8 + $0.95 - $1.05 - $1.10 = $147.06

and my at risk capital is 1.40% or $2.06 a share. That

is. over the next 5 months. I will continue to sell calls, collect

dividends, and sell naked puts to eliminate my risk and produce income,

while at the same time gather any upside beyond $147.06. Note,

I could close this position right now and sell the protective put, which

would reduce my basis further. This is a strategy that accomplishes a

number of things: (1) controls risk, (2) generates income and (3) retains

the big upside move.