The Married Put Strategy is one where both shares of stock are purchased, as

well as an In-the-Money Put with expiration several months in the

future. The longer the time to that expiration, the cheaper is the

cost on a per-month basis. This is a common strategy to control risk

(the downside), while retaining much of the upside reward. In this

article, I'll explore some of the adjustments and their characteristics. To me this is a strategy to control the downside, while getting a decent

return on the cash invested.

Here's an example of the trade we'll consider

here. Shares of SHW were purchased on 01/06/12 for $92.50 and one

contract of June $95 Puts was purchased for every 100 shares at a cost

of $7.70 per share. At that point, our position basis is $100.20,

and for the next 162 days, the lowest price I'll receive for these

shares is the $95--even if SHW shares fall much further, i.e., my

maximum loss possible is $5.20 a share (5.19%). On the other hand,

our upside beyond $100.20 is all ours for this period.

With that said, adjustments can now be made to

reduce the 5.19% downside risk: out-of-the-money calls can be sold

(strike at or above the protective put strike); cash-backed,

out-of-the-money, naked puts can be sold; bear and bull call

spreads can be used; the protective put strike (and time of expiration)

can be changed; and finally dividends can be collected. Here, I'll

assess the trade impact of some of those adjustments for stocks going

up, sideways and down.

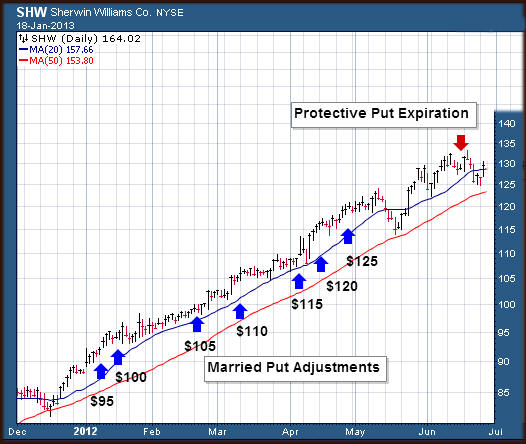

The Steadily Rising Stock (SHW)

As shown in this chart, SHW has risen steadily in 2012. The question is:

What are the plusses and minuses of the Married Put Strategy?

Note, the prices shown are the strike prices of the

puts that were utilized as the shares rose.

Adjusting the Protective Put

The first strategy adjustment that I want to consider is the steady roll to higher strikes as SHW's price rose from 1/1/12 to 6/15/12.

The following table tracks the rise.

-

Rows 6-12 track the initial trade as described above:

300 shares at a cost of $30,060 with three June $95 puts bought at for

$2,310 and total at risk capital $1,560 over the next 162 days

(protective put expires on 6/6/12);

-

Columns B-D track my basis during the trade;

Columns E-H the adjustments; and Columns I-J the trade's returns at each

stage.

Five days later on 1/11/12, SHW's

price has risen to $95.82 (a $3.32 gain), and the first adjustment is made.

-

The June $95 put is sold for $5.60, and the June $100

put is purchased for $8.80;

-

My basis rises to $103.40, while my risk drops to 3.29%;

-

I now have a purchase guarantee of $100.

If I were just long stock shares, I

could close the position for a $3.32 gain. The gain in the married put

position would be $1.22 ($95.82 - $100.20 + $5.60) or 36.75% of what I would

have earned just owning the shares, but that would still be an annualized

88.88%, Of course then, I would also bear all the downside risk.

Notice how increasing the protective put's strike $5 has reduced my at risk

capital to $3.40 per share, though I had to increase my capital by $3.20 per

share.

As SHW continues to rise, the

protective put is adjusted in $5 increments from $95 to $125, and my gain

would be $11.14 per share, a 11.12% gain, while the stock itself gained

40.04%. Clearly, when a stock is steadily rising, I would be better

off just owning the shares, but of course, hindsight is always 20/20.

In each $5 adjustment, I gain $2 utilizing this strategy. On the other

hand, if I had just left the initial position intact rather than making the

adjustments, I would have retained the $100.20 basis and gained $29.34 while

still retaining the downside protection.

|

|